Financial Mistakes Buyers Make: Real Estate Agent Scripts + Preventive Content Ideas

Financial Mistakes Buyers Make

Real Estate Agent Scripts + Preventive Content Ideas

A buyer-safety framework for agents who want to protect approvals, reduce avoidable underwriting friction, and turn financial guardrails into repeatable content.

How agents prevent buyer finance mistakes before closing

The biggest financial mistakes buyers make are opening new credit, adding monthly debt, moving undocumented money, and changing employment without lender clearance. Agents reduce the risk by giving buyers a Do Not Buy checklist, setting a text-before-you-act rule, sending weekly financial alerts, and retargeting checklist visitors with the same safe-to-close message.

- Buyer financial mistakes are usually preventable process failures, not random client behavior.

- The safest agents teach credit, cash-to-close, debt-to-income, and employment guardrails before the first offer.

- A simple Financial Guardrails checklist can become a buyer consult asset, email sequence, social series, and retargeting message.

- The strongest buyer education systems repeat the same warnings across consultation, content, email, and paid follow-up.

Why Buyer Finance Guardrails Pay Off

Financial mistakes buyers make create a predictable operational risk: the buyer looks qualified, keeps shopping, then accidentally changes the lending picture before closing. The business fix is a Financial Guardrails system. It combines first-consult scripts, weekly reminders, a checklist lead magnet, Email Marketing for Real Estate Agents, Social Media Management for Real Estate Agents, and Retargeting and Contextual Ads so the same warning reaches buyers before they make a preventable move.

Buyers do not need a textbook. They need a map. Your map names the handful of mistakes that trigger underwriter rechecks, condition explosions, and last-minute cash gaps. Then you repeat the map in plain language until it becomes buyer muscle memory.

Most agents lose control because they assume the lender will teach these rules in a way the buyer will remember. Lenders communicate risk. Agents must operationalize behavior. That difference is where deals live or die.

- The Credit Freeze Window: the period from pre-approval to funding when new inquiries, new accounts, or balance spikes can trigger lender review.

- Debt-to-Income Creep: the slow rise in monthly obligations that looks small on a receipt but becomes big in underwriting.

- Undisclosed Gift Funds: money that arrives without a clean paper trail and forces extra documentation at the worst possible time.

- The Reserve Shortfall: the cash gap that appears when buyers underestimate closing costs, escrow reserves, and post-close liquidity needs.

Build The Safe-To-Close Guardrail System

High-performance agents treat onboarding as a transaction safety briefing. Your buyer does not wake up hoping to break underwriting. They wake up living their normal life, buying things, taking calls about new jobs, and moving money around. Your onboarding must create productive friction.

Create the first-consult standard

State the rule clearly: no new credit, no big purchases, no job changes, and no major money movement unless the lender clears it first.

Show why the rule exists

Lenders can recheck credit, verify employment again, and request more bank documentation late in the process. Give buyers the cause, not just the command.

Repeat until it sticks

Use one weekly reminder plus a quick text rule for anything that feels like money movement. Consistency protects approvals.

Turn the checklist into content

Deliver the Financial Guardrails checklist as a one-page consult asset and as a web page that buyers can revisit and share.

If you want your language to stay consistent across platforms, borrow the reuse-the-same-building-blocks mindset from Leveraging AI in Real Estate Marketing and Automation for Lead Generation. Then pair each listing discussion on your IDX Real Estate Websites with total monthly carrying cost and cash-to-close context.

Most agents overlook that a buyer's financial mistake is usually a failure of the agent's onboarding process rather than a lack of client intelligence. High-performance operators treat the first 72 hours of a relationship as a Financial Lockdown period where scripts are used to set hard boundaries on spending and credit usage.

Three Buyer Finance Scripts Agents Can Use

These scripts work because they are direct, protective, and operational. Each one gives the buyer a simple rule, a reason behind the rule, and a next step that keeps the agent, lender, and client aligned.

The Gatekeeper Script for the First Consultation

Open“My job is to get you keys, not just show homes. We protect your approval the whole way.”

Boundary“From today until closing: no new credit, no big purchases, no job changes unless the lender clears it first.”

Confirm“If something comes up, you text me before you act. Deal?”

CTA“I will send the Financial Guardrails checklist. Save it and follow it.”

B-roll: desk shot with the checklist visible, calendar reminder titled weekly financial alert, printed checklist hand-off, and lender contact card.

The Credit Lockdown Script for Active Searchers

Hook“One new credit pull can change your rate and your approval.”

Build“Store cards and financing offers show up fast. Lenders can recheck during underwriting.”

Rule“If you want points or a new card, wait until after closing.”

CTA“Want my Do Not Buy list? I will send it today.”

B-roll: direct-to-camera warning, phone screen with credit alert, receipt shot with a financed stamp graphic, and a note that says wait until keys.

The Cash-to-Close Script for Reserves and Gift Funds

Hook“Cash-to-close surprises kill momentum.”

Build“Closing costs, escrow reserves, and moving costs hit at the same time.”

Rule“We track deposits and gift funds early so underwriting stays clean.”

CTA“I will run a cash plan review with your lender this week.”

B-roll: cash-to-close spreadsheet, gift letter checklist, envelope labeled closing costs, and calendar invite titled lender cash review.

Turn The Guardrails Into A Content Engine

Now you turn onboarding into lead generation. This is a preventive content engine: one sequenced series, one checklist lead magnet, one nurture loop, and one retargeting layer. The system attracts buyers who value guardrails and filters out buyers who want vibes instead of standards.

Checklist plus weekly reminder

Build the checklist page, one PDF, one email template, and three posts. Weekly execution is one video, one email, and three posts. The goal is to protect active buyers and capture opt-ins.

Checklist plus paid reminder layer

Build the checklist, a four-week post library, and a retargeting set. Weekly execution is two videos, one email, four posts, plus media when paid retargeting is active.

The four-week Do Not Do It series should run one theme at a time. Week one covers credit, week two covers debt-to-income, week three covers cash and gift funds, and week four covers job changes and income verification risk.

- Credit: new cards, store financing, and credit pulls.

- DTI: new payments, financed purchases, and subscription creep.

- Cash: deposits, transfers, and gift fund documentation.

- Employment: job changes, pay structure shifts, and verification risk.

Publish the series to social, send weekly financial alerts to active searchers, then retarget people who visit your checklist page and your highest-payment listings. Use Retargeting and Contextual Ads to put guardrails in front of intent traffic, not the entire city. For execution quality, model the structure on The Power of Successful Real Estate Agent Digital Media Marketing Campaigns.

| Metric | Window | Range | How to use it |

|---|---|---|---|

| Opt-in rate | 7 days | 3% to 8% | Validate that the checklist headline matches buyer anxiety. |

| Email replies | 14 days | 1% to 3% | Turn common questions into next week's warning post. |

| Retarget CTR | 30 days | 0.7% to 1.6% | Rotate creative weekly if click-through flattens. |

The Financial Mistake Risk Matrix

Use this matrix to preflight every buyer relationship. It also doubles as your content calendar: each row becomes one post, one email, and one short video.

| Mistake category | Impact on loan | Agent preventive action | Best channel |

|---|---|---|---|

| New credit inquiry | Lower scores or new accounts can trigger repricing and reapproval checks. | The Credit Lockdown script with a weekly reminder cadence. | Consultation |

| Large deposits | Unverified funds can delay underwriting through extra documentation requests. | Source of funds audit plus a gift fund template early. | |

| Job change | Income verification can fail when pay structure or employment status shifts. | Career transition consult with the lender before any change. | In-person |

| Big purchases | New payments can push debt-to-income above approval thresholds. | Wait until keys campaign with one rule repeated weekly. | Social media |

The 10-Point Buyer Financial Safety Audit

Use this audit to verify your buyer education process. It protects your transactions and keeps your messaging consistent across consultations and content.

- Deliver a Do Not Buy list in the first consult and confirm the buyer can repeat the rule back.

- Define the Credit Freeze Window and state the standard: no new inquiries until after closing.

- Explain Debt-to-Income Creep with one payment example and the underwriting impact.

- Confirm down payment funds, reserves, and closing costs as three separate buckets.

- Ask about gift funds early and collect documentation before offers are written.

- Warn against large deposits and require a text rule before money moves.

- Set a job change rule and route any employment decisions through the lender first.

- Frame total monthly carrying cost for each target home, not just list price.

- Install a weekly financial alert cadence so buyers stay compliant while shopping.

- Retarget checklist visitors and high-intent listing viewers with the same rules and scripts.

How One Agent Turned Buyer Risk Into A Financial First System

An agent in a high-price market lost three deals in one quarter due to buyers making large retail purchases during escrow. The pattern was not random. The agent never set a spending boundary early, so buyers treated pre-approval like a suggestion.

They pivoted to a Financial First strategy and built a local page targeting the phrase “financial mistakes buyers make in the city.” They integrated a Financial Guardrails video series into their social content, then used Retargeting and Contextual Ads to show warnings to leads who viewed higher-payment listings.

Over time, the agent saw fewer buyer-created financing problems and stronger lead-to-close discipline. The key change was not more content volume. It was clearer standards, earlier education, and a repeatable reminder system that protected current escrows while the agent focused on appointments.

Make Financial Guardrails Part Of Your Buyer Brand

Being the guardian of the transaction is not a personality trait. It is a system. When you lead with guardrails, you reduce chaos and attract buyers who value standards.

Record one 60-second warning video on the No New Credit rule today. Then map it into a four-week series with scripts, a checklist page, weekly email alerts, and retargeting reminders that keep buyers safe to close.

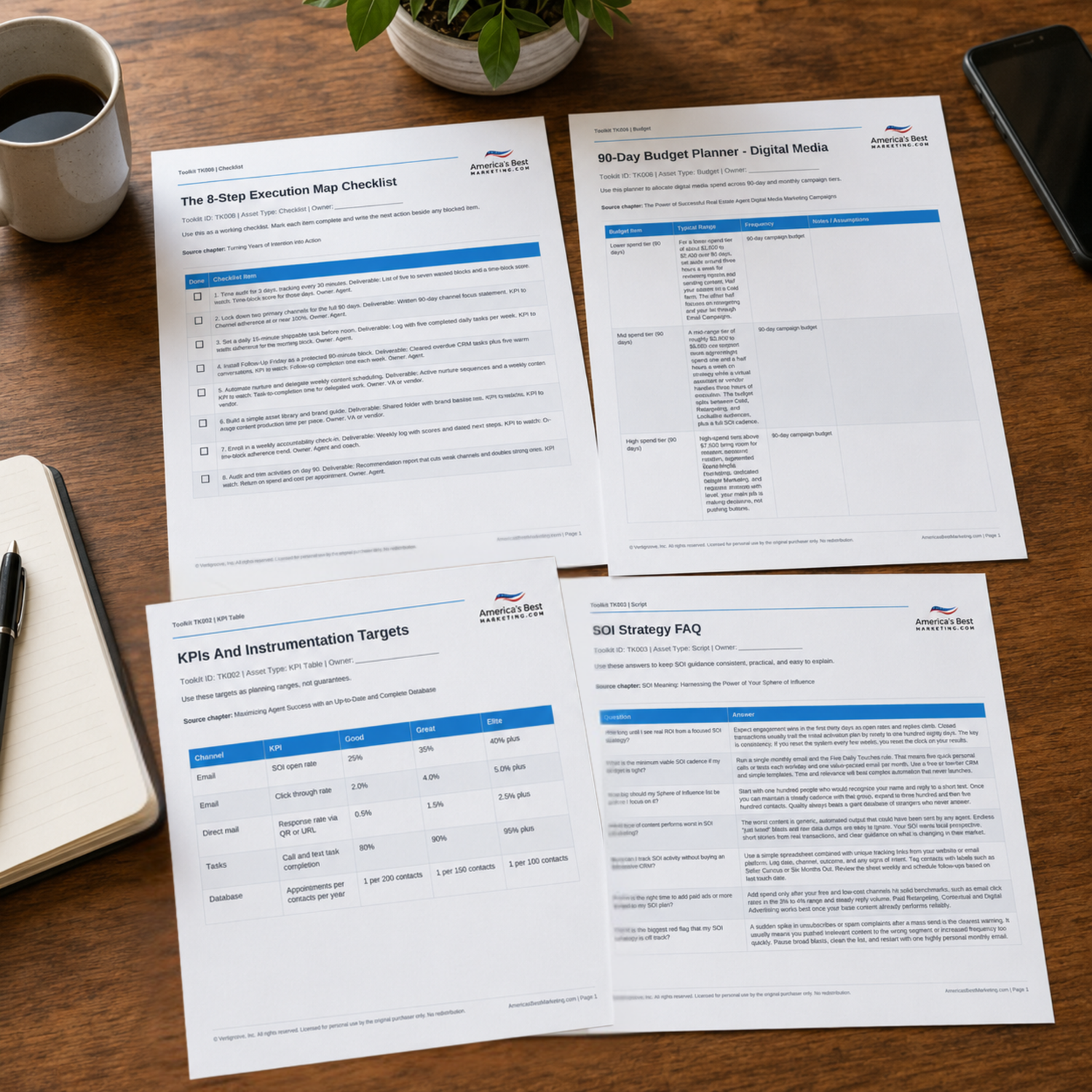

Download The Buyer Financial Guardrails Toolkit

Use the download to turn this article into working assets: buyer scripts, safety checklist, KPI table, risk matrix, budget plan, and the four-week Do Not Do It content sequence.

Download the Toolkit ZIPRecommended Reads

Recommended Reads for Real Estate Agents

These articles help agents turn client questions, local guidance, marketing channels, and follow-up into a more useful content system.

Winning the Rental Market: Strategies for Converting Renters into Homebuyers

Bring more structure to renter-to-buyer strategy so every touchpoint supports visibility and trust.

Read article

How to Convert Online Buyer Leads into Appointments and Closings

Bring more structure to convert online buyer leads into appointments and closings so every touchpoint supports visibility and trust.

Read article

Live Streaming Q&As for Real Estate Agents: Topics, Scripts, and Promotion Plan

Create video content with clearer scripts, simpler formats, and a cadence agents can actually maintain.

Read article

Top Mistakes Agents Make When Buying Real Estate Leads and the Multi-Channel Strategy That Actually Works

Bring more structure to lead buying mistakes so every touchpoint supports visibility and trust.

Read articleBuyer Finance Questions Agents Should Be Ready To Answer

How long does it take to see ROI from educational content?

Look for early signals within two to four weeks: opt-ins, replies, and consult requests. Closings take longer, so track leading indicators first, then tie them back to appointments and signed buyer agreements.

What is the most common mistake buyers make in a high-interest rate environment?

They shop payment last. Buyers focus on list price and ignore rate sensitivity, escrow, and insurance. Teach total monthly carrying cost early and set a no-new-debt rule while they shop.

Can a buyer open a credit card if they have a high score?

High scores do not make someone immune. A new inquiry, a new account, or a new balance can still change pricing and conditions. The safe standard is simple: wait until after closing unless the lender explicitly clears it.

How should an agent explain debt-to-income ratios without sounding technical?

Use a plain framing: every new monthly payment reduces buying power. Give one example using a car payment and show the impact on approval range. Keep it behavioral and route specifics to the lender.

How often should weekly financial alerts go out during the search period?

Once per week is enough. Keep it short, repeat the same four rules, and add one example. Consistency beats volume because the goal is compliance.

What should an agent do if a buyer already made a big purchase during escrow?

Move fast and involve the lender immediately. Collect the purchase terms, timing, and payment details, then pause additional spending. Reduce variables and document the path back to approval.

How do you turn this into lead generation without sounding salesy?

Lead with protection. Offer the checklist, then follow with calm reminders and a simple affordability review. Buyers book calls when they feel safe, not when they feel pitched.

Next step

Build the System Behind the Advice

Continue from one useful article into the larger ABM ecosystem: the book series for strategic depth and the full marketing program for done-for-you execution.

View the Book Series

Explore the America’s Best Real Estate Agent Marketing System books for a deeper strategic framework around visibility, referrals, listings, lead generation, and growth.

View the Book Series

See Full Marketing Program

See how AmericasBestMarketing.com runs real estate blog writing, social media, listing marketing, email, direct mail, and retargeting as one managed system.

See Full Marketing Program